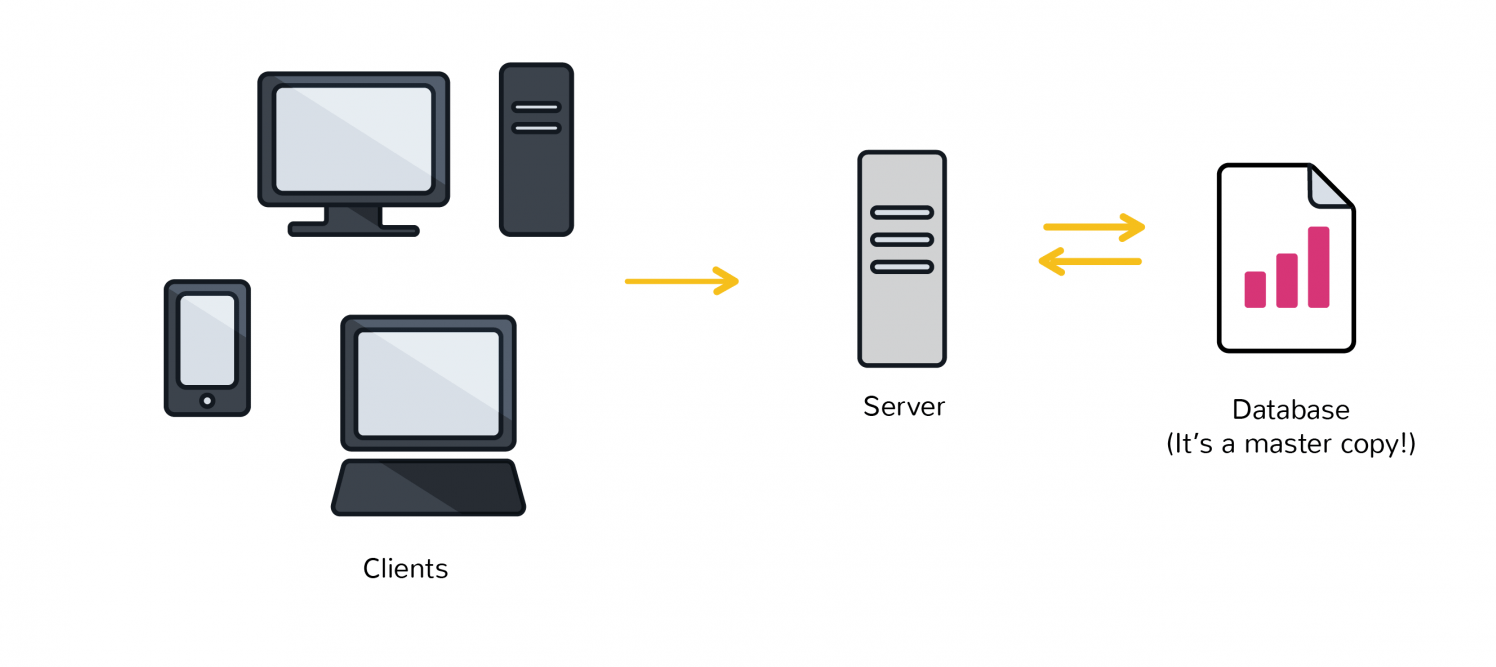

Traditional Internet

A standard website’s backbone is similar to the highly protected and centralized databases that governments or banks or insurance companies keep today. Control of centralized databases rests with their owners, including the management of updates, access and protecting against cyber-threats.

The distributed database created by blockchain technology has a fundamentally different digital backbone. This is also the most distinct and important feature of blockchain technology.

A website’s ‘master copy’ is edited on a server and all users see the new version. When a website gets hacked, everyone sees the hacked copy. If the information in the database is hacked, deleted, corrupted or changed, the website operates on the incorrect data.

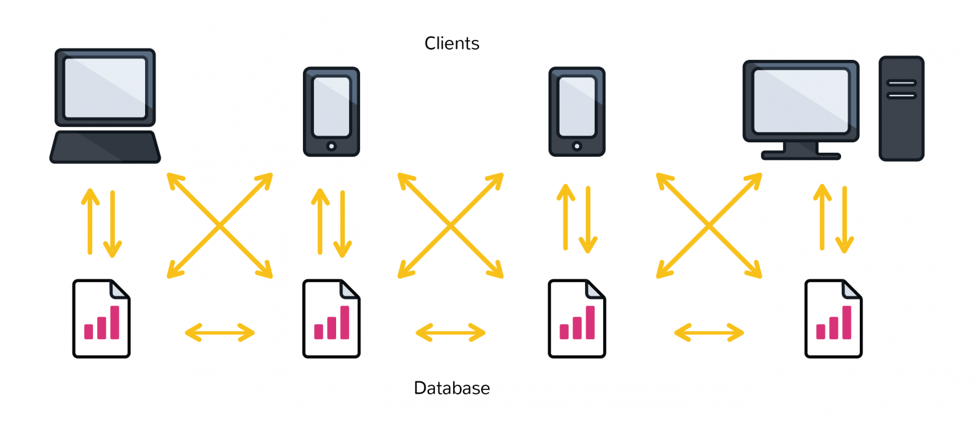

Using blockchain technology, every node in the network comes to its own conclusion, each updating the record independently, with the most popular record becoming the de-facto official record in lieu of there being a master copy.

Blockchain Internet

Using blockchain technology, transactions (changes) are broadcast, and every node is creating their own updated version of events.

It is this difference that makes blockchain technology so useful – It represents an innovation in information registration and distribution that eliminates the need for a trusted party (a main server-based database or master copy) to facilitate digital relationships.

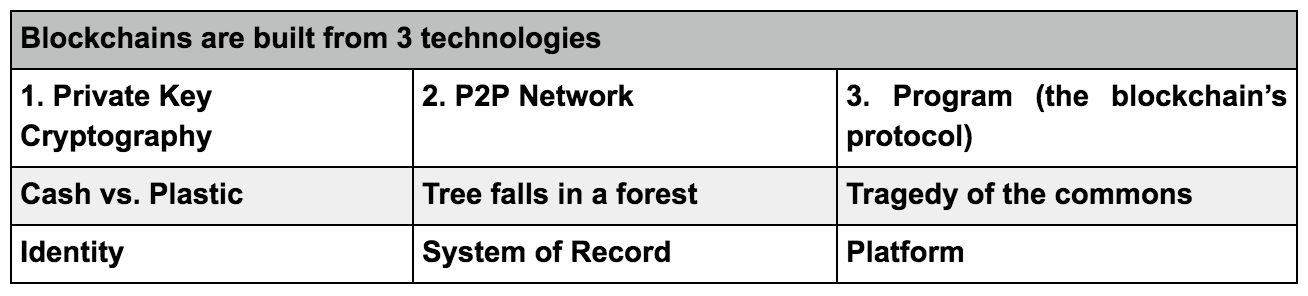

Blockchain technology is not an entirely new creation, it is a combination of proven technologies applied in a new way. It was the particular orchestration of three technologies (the Internet, private key cryptography and a protocol governing incentivization) that makes this idea so useful and revolutionary.

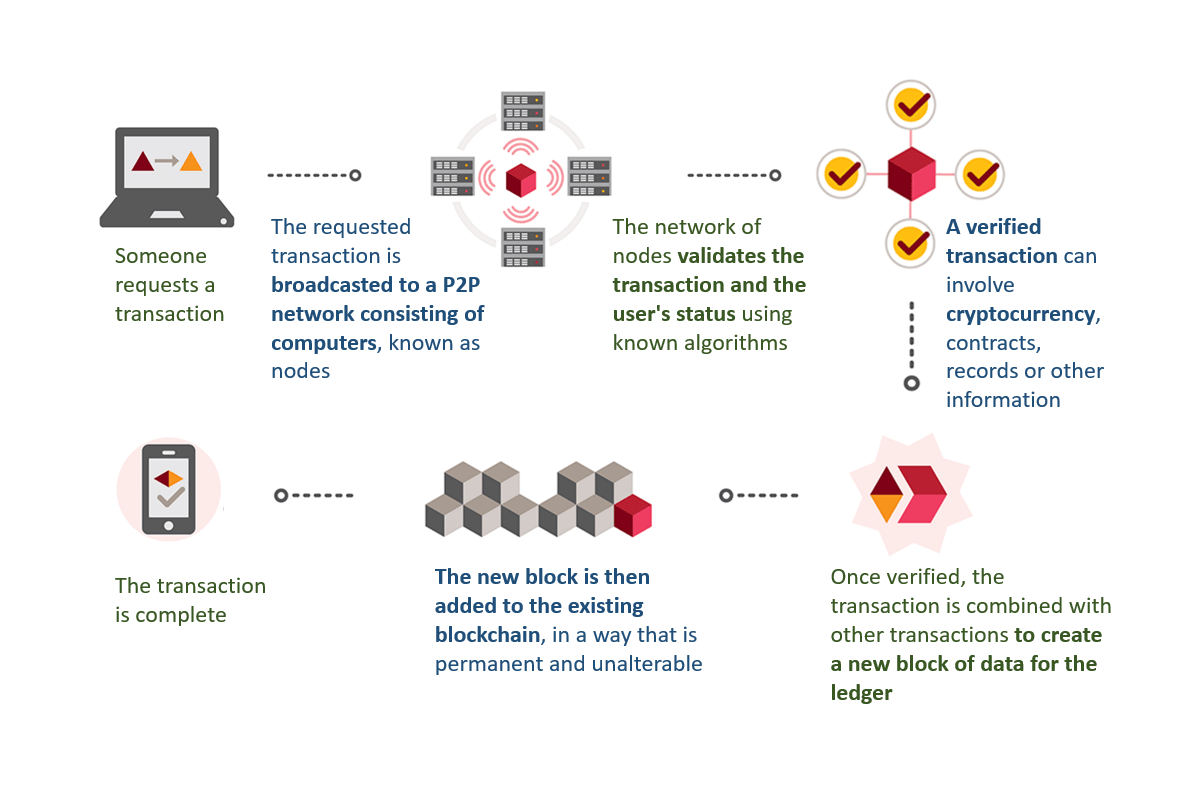

Using blockchain technology, data is encrypted and added to a permanent ledger that is then processed by many independent nodes. The integrity and continuity of the data is ensured using this process because even if one node is compromised, the majority of nodes will agree on the CORRECT data.

Composition of the Blockchain

The result is a system for digital interactions that does not need a trusted third party. The work of securing digital relationships is implicit — supplied by the elegant, simple, yet robust network architecture of blockchain technology itself.

Defining digital trust

Trust is a risk judgement between different parties, and in the digital world, determining trust often boils down to proving identity (authentication) and proving permissions (authorization).

Put more simply, we want to know, ‘Are you who you say you are?’ and ‘Should you be able to do what you are trying to do?’

In the case of blockchain technology, private key cryptography provides a powerful ownership tool that fulfills authentication requirements. Possession of a private key is ownership. It also spares a person from having to share more personal information than they would need to for an exchange, leaving them exposed to hackers.

Authentication is not enough. Authorization – having enough money, broadcasting the correct transaction type, etc – needs a distributed, peer-to-peer network as a starting point. A distributed network reduces the risk of centralized corruption or failure.

This distributed network must also be committed to the transaction network’s recordkeeping and security. Authorizing transactions is a result of the entire network applying the rules upon which it was designed (the blockchain’s protocol).

Authentication and authorization supplied using blockchain technology allow for interactions in the digital world without relying on (expensive) trust. Today, entrepreneurs in industries around the world have woken up to the implications of this development – unimagined, new and powerful digital relationshionships are possible.

Blockchain technology is often described as the backbone for a transaction layer for the Internet, the foundation of the Internet of Value.

In fact, the idea that cryptographic keys and shared ledgers can incentivize users to secure and formalize digital relationships has imaginations running wild. Everyone from governments to IT firms to banks is seeking to build this transaction layer.

Authentication and authorization, vital to digital transactions, are established as a result of the configuration of blockchain technology.

The idea can be applied to any need for a trustworthy system of record.

What Are Some Uses for Blockchain Technology?

Payment Systems

Payments are timestamped and permenantly recorded in the blockchain ledger. Payment processing costs are reduced significantly and funds are transferred instantly.

Employee Benefits

Employee benefits such as PTO can be accumulated and used through a secure process. Transactions are timestamped, recorded, and deducted from the employee’s account.

Claims Processing

Insurance claims processing is streamlined, reducing claims processing time and costs associated with insurance claim fraud. Claims workflow and payments are recorded.

Records Management

Documents stored on the blockchain can be accessed by authorized parties. Records are timestamped, access and additions or changes are recorded in the ledger.

We are Blockchain Developers! Want More Information?

Blockchain and Distributed Ledger Technology (DLT) is the biggest advancement since the Internet. It empowers transparency, privacy, and security, and has the potential to disrupt entire industries in the near future.

Learn how blockchain is relevant to your industry, discover the biggest opportunities and obstacles facing your business – and what to do about them!